GST registration is mandatory for many businesses operating in India. However, there are situations where a business may no longer require GST registration due to business closure, low turnover, restructuring, transfer of ownership, or voluntary deregistration.

In such cases, taxpayers must apply for GST registration cancellation through the GST portal to avoid unnecessary compliance requirements, late fees, penalties, and continuous return filing obligations.Cancelling GST registration is not simply about stopping business activities. Businesses must complete the proper GST cancellation procedure, settle pending liabilities, reverse applicable Input Tax Credit (ITC), and file the final GST return (GSTR-10).

This comprehensive guide explains:

- What GST cancellation means

- Who can cancel GST registration

- Reasons for GSTIN cancellation

- GST cancellation rules

- Documents required

- Step-by-step GST cancellation process

- GSTR-10 filing requirements

- Common mistakes to avoid

- GST cancellation FAQs

GST Cancellation Quick Summary

| Particulars | Details |

| Purpose | Cancellation of GST registration |

| Governed By | CGST Act & GST Rules |

| Applicable To | Registered taxpayers |

| Main Form | GST REG-16 |

| Cancellation Order | GST REG-19 |

| Final Return | GSTR-10 |

| Filed Through | GST Portal |

| Initiated By | Taxpayer or GST Department |

| Main Reasons | Business closure, turnover below threshold, business transfer, restructuring |

| Time Limit for Final Return | Within 3 months |

What is GST Cancellation?

GST cancellation refers to the legal process of deactivating a GST registration (GSTIN) when a business no longer needs to remain registered under GST laws. After cancellation, the business cannot collect GST, issue GST invoices, or claim Input Tax Credit (ITC).Additionally, taxpayers no longer need to file regular GST returns after the cancellation becomes effective. However, businesses must still file the final return in GSTR-10 within the prescribed timeline.

In simple terms, GST cancellation ends the taxpayer’s legal GST compliance responsibilities unless a new registration is obtained later.

Why is GST Registration Cancellation Important?

Proper GST cancellation helps businesses avoid unnecessary compliance burdens and legal complications. Moreover, it prevents taxpayers from receiving notices for non-filing of GST returns after business operations stop.

Benefits of GST Cancellation

- Avoids continuous GST return filing

- Prevents late fees and penalties

- Reduces administrative and compliance burden

- Ensures proper legal closure

- Helps avoid GST department notices

- Simplifies business restructuring processes

Who Should Read This GST Cancellation Guide?

- Small business owners

- Startups

- Proprietors

- Partnership firms

- Freelancers and consultants

- E-commerce sellers

- Chartered accountants

- Businesses undergoing mergers or restructuring

- Taxpayers planning business closure

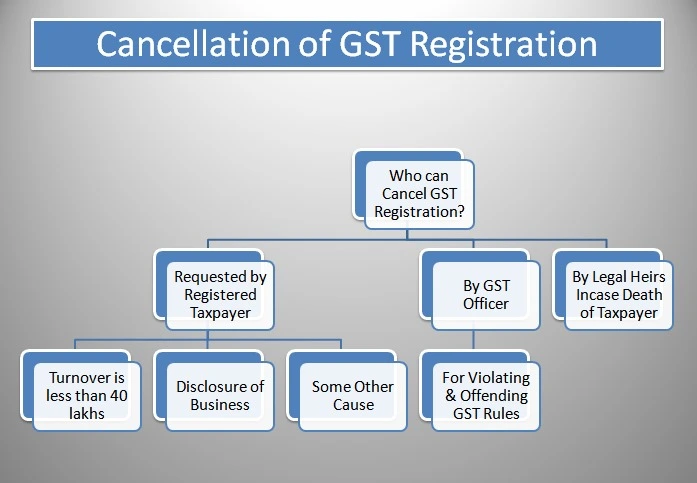

What are the Reasons for GST Registration Cancellation?

Businesses may apply for GST cancellation for several valid reasons under GST law.

1. Permanent Closure of Business

Businesses should cancel GST registration when they permanently stop operations. Otherwise, they may continue receiving GST compliance notices and return filing obligations.

2. Turnover Falls Below GST Threshold Limit

Additionally, businesses whose annual turnover falls below the mandatory GST registration threshold may apply for cancellation. This helps reduce unnecessary compliance costs and filing responsibilities.

3. Transfer, Merger, or Sale of Business

Businesses may also require GST cancellation when ownership changes due to transfer, merger, inheritance, or sale.

Example:

A father transfers his manufacturing business to his son. In this situation, the existing GST registration becomes invalid, and the new owner must obtain a fresh GSTIN.

4. Change in Business Constitution

Businesses often need a new GST registration after changing their legal structure.

Common Examples

- Proprietorship converted into partnership

- Partnership converted into company

- LLP conversion

- Private limited company restructuring

5. Business Providing Only Exempt Supplies

If a business exclusively deals in GST-exempt goods or services, GST registration may no longer be required.

6. Voluntary GST Registration No Longer Required

Some businesses voluntarily obtain GST registration to claim ITC or work with larger clients.If these benefits are no longer necessary, GST cancellation can be requested.

7. Reducing GST Compliance Burden

Businesses with minimal operations may find GST compliance expensive and time-consuming.Cancelling GST registration helps reduce filing obligations and administrative work.

Types of GST Cancellation

GST cancellation can be initiated either by the taxpayer or by the GST department.

Voluntary GST Cancellation

Voluntary GST cancellation allows registered taxpayers to cancel their GST registration when it is no longer necessary. Businesses commonly choose this option after permanent closure, operational discontinuation, or reduced turnover below the GST threshold limit.

Moreover, taxpayers may voluntarily cancel GST registration after changing the business constitution or restructuring operations.

When Can Businesses Apply for Voluntary GST Cancellation?

Businesses may apply for voluntary GST cancellation in situations such as:

- Permanent business closure

- Business discontinuation

- Turnover below threshold limit

- Conversion of business structure

- Transfer of business ownership

- Reduced business activities

Benefits of Voluntary GST Cancellation

Voluntary cancellation offers several advantages:

- Reduces compliance costs

- Eliminates monthly return filing

- Prevents future penalties

- Simplifies legal closure procedures

- Avoids unnecessary GST notices

Department-Initiated GST Cancellation

The GST department can cancel a taxpayer’s registration when serious non-compliance or fraudulent activities occur.

Reasons Why the GST Department Cancels Registration

The department may cancel GST registration for reasons such as:

- Continuous non-filing of GST returns

- Fake invoicing activities

- Wrongful ITC claims

- Fraudulent registration

- Business not operating from the registered address

- Violation of GST provisions

Show-Cause Notice Before Cancellation

Before cancellation, the GST department usually issues a show-cause notice requesting clarification from the taxpayer. The taxpayer must respond within the specified timeline.

However, if the taxpayer fails to provide a satisfactory response, the department may proceed with cancellation.

Documents Required for GST Cancellation

- GST registration certificate

- PAN card

- Aadhaar of authorized signatory

- Proof of business closure

- Transfer or merger agreement

- Stock details and capital goods statement

- ITC reversal details

- Latest GST return acknowledgment

- Payment proof for pending liabilities

Accurate documentation helps businesses avoid delays, notices, and rejection.

How to Cancel GST Registration Online (Step-by-Step Process)

Step 1: Login to GST Portal

Visit the GST portal and log in using your GST credentials.

Step 2: Select GST Cancellation Application

Navigate to: Services → Registration → Application for Cancellation of Registration

Step 3: Choose Reason for GST Cancellation

- Business closure

- Turnover below threshold

- Transfer of business

- Change in constitution

- Voluntary cancellation

Step 4: Enter Required GST Cancellation Details

- Date of business closure

- Stock and capital goods details

- ITC reversal amount

- Outstanding tax liabilities

“Accurate details help avoid rejection or notices.”

Step 5: Upload Supporting Documents

Attach the required supporting documents based on the cancellation reason.

Step 6: Verify and Submit Application

- DSC (Digital Signature Certificate)

- E-sign

- OTP verification

After submission, an Application Reference Number (ARN) is generated for tracking.

Step 7: GST Officer Review & Approval

Finally, the GST officer reviews the application and supporting documents. If everything is correct, the officer issues Form GST REG-19 confirming cancellation approval..

Common Mistakes to Avoid During GST Cancellation

Many GST cancellation applications are delayed due to avoidable errors.

- Applying without filing pending returns

- Incorrect stock declaration

- Wrong ITC reversal calculation

- Uploading incomplete documents

- Ignoring GST department notices

- Missing GSTR-10 filing

- Incorrect business closure date

“Preparing documents and compliance details in advance helps ensure faster approval.”

GST Cancellation vs GST Suspension

| Basis | GST Cancellation | GST Suspension |

| Meaning | Permanent closure of GST registration | Temporary suspension |

| GST Return Filing | Not required after cancellation | Suspended temporarily |

| GSTIN Status | Deactivated permanently | Temporarily inactive |

| ITC Claim | Not allowed | Restricted during suspension |

Can GST Cancellation Be Revoked?

Yes. Taxpayers may apply for revocation if the GST department cancels their registration under eligible circumstances.

However, businesses must usually submit the revocation application within the prescribed time limit after receiving the cancellation order. Additionally, taxpayers must complete pending compliance requirements before seeking revocation approval.

Latest GST Cancellation Updates for 2026

- Increased scrutiny on inactive GST registrations

- AI-based GST compliance monitoring

- Faster GST cancellation verification process

- Improved GST portal automation

- Enhanced mismatch detection for ITC reversal

Businesses should regularly monitor GST notifications and compliance updates.

“Need help with GST registration cancellation? Contact our GST experts for quick and hassle-free assistance.”

Conclusion

Understanding the GST registration cancellation process helps businesses avoid penalties, reduce compliance burdens, stop unnecessary GST return filing, and ensure smooth legal closure. By filing pending returns, submitting accurate details, reversing applicable ITC, and filing GSTR-10 on time, businesses can complete the process smoothly and remain GST compliant.

Frequently asked questions about GST Cancellation

Yes. GST registration can be canceled online through the GST portal by submitting Form GST REG-16 along with the required business details and supporting documents. Taxpayers must provide reasons for cancellation, stock details, and pending liability information. After verification by the GST officer, the cancellation order is issued online.

Yes. GSTR-10 is the final GST return that must be filed after GST registration cancellation in most cases. It includes details of closing stock, Input Tax Credit (ITC) reversal, and pending tax liabilities. Filing GSTR-10 helps officially close the taxpayer’s GST account and complete final compliance requirements.

If GST returns are not filed without canceling GST registration, the taxpayer may receive GST notices, late fees, interest, and penalties from the GST department. Continuous non-filing can also lead to department-initiated cancellation and compliance issues. Businesses should properly cancel GST registration to avoid future legal complications.

The GST cancellation process generally takes around 15 to 30 days depending on document verification, pending returns, and GST officer approval. Delays may occur if incorrect information or incomplete documents are submitted. Filing accurate details and clearing pending liabilities can help speed up the approval process.

Yes. Taxpayers who voluntarily registered under GST can apply for cancellation if GST registration is no longer required for their business operations. Businesses with lower turnover or discontinued activities often choose voluntary GST cancellation to reduce compliance burdens and return filing obligations.

Common documents required for GST cancellation include the GST registration certificate, PAN card, Aadhaar of the authorized signatory, proof of business closure, stock details, and ITC reversal calculations. Additional documents may be required depending on the reason for cancellation and business structure.

Yes. GST cancellation applications may be rejected if pending GST returns, unpaid liabilities, incorrect stock details, or incomplete documents exist. The GST officer may also issue notices seeking clarification before approval. Ensuring proper compliance and accurate documentation helps reduce rejection risks.